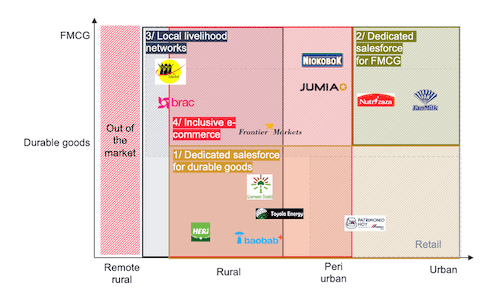

Last-mile distributors have found innovative ways to affordably reach consumers living in underserved and/or hard-to-reach areas. As Lucie Klarsfeld McGrath, Jeanne Charbit and Joana Furquim at Hystra explain, these companies use many different last-mile distribution models, tailored to different goods and locations. They discuss the revenue and impact potential of four common models, assessing when they are most relevant, exploring their limitations and optimal conditions for success, and highlighting the key challenges and questions they face moving forward.Last-mile distributors (LMDs) provide access to life-changing products and create local jobs in underserved and/or hard-to-reach areas. The term “last-mile” covers a range of locations, from urban slums to rural areas. LMDs have found innovative ways to affordably reach consumers living at the last mile, including by reducing transportation costs, leveraging local networks — and using digital resources to do so. There are many different last-mile distribution models, tailored to different goods and locations. These models vary in revenue and impact potential, and they face different challenges and leverage different best practices to address them. Distinguishing them can allow LMDs to better define which model is best suited to their objectives, while also helping funders, product manufacturers and service providers to develop offers tailored to the needs of last-mile distributors facing specific challenges inherent to their model. Figure 1: Geographical areas and types of goods covered by four types of last mile distributors. In a 2021 NextBillion article, “Creating Sustainable Last-Mile Distribution for Beneficial Products: Two Network Archetypes (and How They Can Scale Up)” we at Hystra identified two archetypes of last-mile distributors: “Dedicated Salesforce” and “Local Livelihoods,” based on data provided by Global Distributors Collective members and previous LMD research. Our experience in the subsequent years has enabled us to further refine these categories into four models, splitting the “Dedicated Salesforce” model between: 1.) Dedicated Salesforce for Durable Goods and 2.) Dedicated Salesforce for Fast-Moving Consumer Goods (FMCGs); and splitting the “Local Livelihoods” model between 3.) Local Livelihoods Networks and 4.) Inclusive E-Commerce. This last model is a recent development, based on the growing use of digital tools among some well-established local livelihoods networks — and, conversely, on the efforts of traditional e-commerce platforms to expand into more rural areas by leveraging local livelihoods networks for intermediation. This article explores each of these models, assessing when they are most relevant, describing their optimal conditions for success, limitations, revenue and impact potential, and highlighting the key challenges and questions they face moving forward. Dedicated salesforce for durable goods This model is relevant when companies adopt a dedicated salesforce to sell an innovative and/or complex product — or a range of similar products — such as improved cookstoves, solar home systems, solar pumps or water filters. It is well-suited to places with limited competition, and remains relevant over the long term if the direct salesforce model continues to deliver distinct value to consumers, such as providing after-sales service or ensuring the delivery of heavy products to remote locations. For example, Toyola Energy and Feu Vert Bénin sell improved cookstoves across West Africa through local retailers in peri-urban areas and direct delivery in rural areas, offering a try-before-you-buy model in rural markets. Best practices include: Properly selecting and training full-time or nearly full-time sales agents, and remunerating them with competitive salaries above what they could earn from similar jobs. In denser areas and/or more mature markets, this model can be complemented or progressively replaced by existing specialized local shops targeting a specific product category, with employees trained to sell these products (e.g., agro-shops for solar pumps). Maintaining a long-term client relationship, first by systematically ensuring that products work well, which encourages positive word of mouth, then by creating a system to leverage referrals from past clients — and by promoting upselling (e.g., through follow-up calls or visits, or referral schemes). Common mistakes include: Opting to work with local agents who have limited mobility, often as part of an income-generation or “empowerment” strategy, as seen in the local livelihoods model. These agents quickly saturate their sales zones, and while they might be able to sell additional durable goods within the same area, introducing new, complex products requires costly retraining and capacity-building efforts. Given their small catchment areas, the resulting sales volume is often insufficient to justify the expense of expanding the product basket. Instead, local people can be recruited to aggregate pre-sales in exchange for a commission, allowing the LMD to scale back the activities of the sales agents in these communities while several sales are guaranteed. The crucial difference between this approach and the local livelihood model (which we have never seen self-sustain) is the amount of time and money spent on utilizing these local sales aggregators, which is non-existent in this model, as agents simply leverage existing clients to serve as aggregators, without providing any formal company training or support. Selling multiple categories of complex products simultaneously or piggybacking on an existing specialized salesforce. These approaches are challenging, since agents would require extensive new skill development to effectively sell additional products, adding significant costs. Indeed, networks offering diverse, complex product baskets tend to achieve lower sales per agent compared to those focused on a single product category at a time — and often find that their best agents have opted to specialize in the product they were most comfortable with. Revenue and impact potential: These LMDs can achieve sales of over $20,000 per year (per full-time equivalent), allowing them to pay agents above US $2,500 per year. This, in turn, motivates agents to remain in the salesforce, and limits the LMDs’ HR (e.g., recruitment and training) costs. Key questions and challenges: Tactical or operational: LMDs should determine how to institutionalize best practices for maximizing sales, particularly by leveraging their initial satisfied clients to maximize penetration in an area before competition comes in. Strategic: LMDs should also assess how to transition agents once products have become more widespread: Should they be moved to wholesale roles selling to retailers, or take on new products? Dedicated salesforce for FMCGs This model is relevant when companies launch new FMCGs, as a direct sales network can replace some of the fixed costs of a traditional advertising and promotions budget. Sales agents can also gather early consumer feedback and push consumption frequency. Additionally, this model is fit for products that require an otherwise non-existent infrastructure (e.g., portable refrigerators for products that require a cold chain, or hot thermoses for warm drinks). Best practices include: Working with full-time or nearly full-time sales agents who are mobile or semi-mobile, with a predictable route that allows them to serve the same customers daily. Transitioning sales agents from serving customers directly to also serving local shops once products become mainstream (e.g., Nutri’zaza, which initially sold its fortified infant porridge Koba Aina through door-to-door women vendors, then expanded to retail shops as growing demand from families made the product mainstream). Moving to a traditional distribution and retail model (e.g., Grameen Danone, which originally distributed fortified yogurt through a social business model in Bangladesh, but later transitioned to traditional retail and distribution channels as demand grew). Ensuring that the infrastructure for product sales is truly differentiating, providing continued value-add over time to consumers or generating positive externalities to the business (e.g., the “free” visibility provided by branded sales agents and infrastructure, which limits the need for other marketing costs). Common mistakes include: Selling in areas that are not dense enough to generate sufficient revenues from FMCGs to justify not only the sales agents’ commission but also the management costs of recruiting, training and supporting agents (e.g., rural areas). Keeping a dedicated business-to-consumer salesforce once its unique value-add fades (e.g., when products become available in shops). Revenue and impact potential: These LMDs can achieve sales above $10,000 per year (per full-time equivalent), allowing them to pay agents above US $1,000 per year (since the usual margin they would have spent on distributor and retailer costs can go toward paying the salaries of agents, who eliminate the need for both of those expenses). Key questions and challenges: Strategic: When can the intangible value brought by these sales networks (e.g., enhancing the company’s public image or strengthening its brand, providing marketing savings, increasing the potential for co-funding from donors focused on boosting livelihoods or women’s empowerment) equal or exceed the potential extra costs that come with them (e.g., additional distribution and management expenses)? Operational: How can LMDs design sales agent routes to ensure they each have a sufficient catchment area and maximize their sales? How can they maintain (best) sales agent performance over time? Local Livelihoods Networks This model is relevant when product access is a challenge across sectors (i.e., in remote rural areas). In this model, the head organization (often a social enterprise or NGO) trains and supports village-level entrepreneurs, often women, in becoming sales points for an array of (not too complicated, not too expensive) beneficial products. Historically, this model has been in large part donor-funded, with specific objectives around women’s empowerment and/or a dedicated health impact objective (e.g., door-to-door sales of nutrition products). Following this approach, between 2020 and 2024, with support from the Gates Foundation, Hystra helped RSPN test a women-led last-mile commercial model in Pakistan that distributed health, nutrition and hygiene products: It demonstrated strong demand but — like all other models we have seen in this category — could not cover all of its costs via product margins only. Best practices include: Leveraging the local infrastructure to the maximum, creating local wealth that can be reinvested in products and services sold locally. Limiting scope to beneficial products (or at least to products that “do no harm,” e.g., no cigarettes and alcohol). Building in recurring philanthropic and/or public funding to provide health services and benefits beyond what local villagers can afford. Partnering with organizations looking to explore a new market, test a new product or business model, or reach remote communities, to create new revenue streams for local agents and the head office. Common mistakes include: Failing to establish a reliable and responsive supply process (e.g., by not addressing the need for business skills and mindsets that can be missing in NGOs), despite the critical role of consistent supply in building trust with local agents and end-clients. Trying to reach sustainability only by selling products to villagers, as the available resources in those areas are not enough to cover the model’s operational costs. Revenue and impact potential: These LMDs can achieve sales of US $6,000-7,000 per year at best (per full-time equivalent) and require ongoing subsidies. Besides generating income opportunities for local entrepreneurs, this model allows local villagers to save the money they would otherwise spend on transport to access products. Key questions and challenges: Tactical or operational: What local resources can be tapped at limited costs by these LMDs? In particular, how can they leverage local human resources, given people’s often-limited education levels or available time? Strategic: Are there enough funds in rural areas to sustain this model without external funding — and if so, what is the “right” product basket to tap into those local funds? If not, what is the optimal mix of revenue streams, including payment from third parties (e.g., selling data or marketing, or obtaining pay-for-impact grants/investments)? Is inclusive e-commerce the future of these models, as they work toward improved sustainability? Inclusive e-commerce This model is relevant when countries have sufficient connectivity and affordable data, including in rural areas. These LMDs either started as traditional e-commerce companies aiming to expand their reach, or as socially driven businesses looking to improve their sustainability. Traditional e-commerce companies, like Niokobok and Jumia, have used data to optimize delivery to remote areas and added physical intermediaries to expand their reach. Niokobok, launched in 2012, enables diaspora members to buy products from abroad, which are delivered to their families in Senegal, while Jumia serves 5.4 million active customers across Africa. In contrast, companies that are “social from the start” serve remote areas at the outset and add digital tools to their

Related Posts

Technical Analysis: 4 Stocks with signs of death crossovers to keep an eye on

HDFC Bank & 3 other fundamentally strong stocks trading above 200 DMA to keep an eye on

Falling Channel Breakout: Multibagger NBFC Stock Shows Bullish Momentum on Daily Chart

4 Fundamentally strong stocks to buy for an upside potential of up to 36%; Do you hold any?

0 responses on "Comparing Four Last-Mile Distribution Models: Best Practices and Common Pitfalls in Reaching Rural Customers"